Your Top 11 401k Questions, Answered

Let me ask you a question.

If I asked you right now at what age you want to live out the rest of your life doing whatever you want to do, without slaving away your days, what would your answer be?

Would it be 65… 60… 55… even 50 or less?

Have you ever sat down and thought about it? If not, I challenge you to make that a life priority, because whatever that age is, you’re going to need a healthy retirement savings to achieve it.

I’ll tell you right now that whatever age you want it to be, it’s within reach, as long as you make the correct life choices to get there.

I ask a lot of people this question, and I quite frequently get answers in the 50s, which is awesome!

But when I ask those same people how they’re going to do it, I usually hear back something to the tune of “I haven’t figured that out yet,” or “it’ll work out.”

No… it won’t. Not unless you get serious and do something about it.

This is something you have to get intentional with. It’s not going to happen on it’s own and it’s not going to happen by saving what is left over.

Isn’t it interesting that there is such a difference between what people say they want, and what their behavior shows?

Simply sitting back and hoping that everything will work out isn’t a plan. It’s a strategy for failure.

Even if you don’t know exactly when you’re going to retire, or exactly how much money you’ll need to do it, you can still get started now until you do figure that out.

(PS: Here’s a great post by Mr. Money Mustache with a very simple way to figure this out.)

One of the most popular ways to set up a retirement plan is to enroll in your employer 401k. Personally, my 401k is by far my largest investment account on my road to becoming a millionaire as well as retiring not too long after.

We’ve talked plenty about the massive benefits of a 401k. You can check out any of the posts below for more on that.

- The Incredible Wealth Creating Power of the 401k Quadruple Threat

- Seven Awesome Things to Do With Your Extra Money Without Blowing It

- The Only Three Money Principles You Need to Get Rich

What I’d like to do now is help you eliminate some of the uncertainty you might have with your 401k so you can get started without worrying that you’re going to make a mistake.

One of the top reasons people don’t invest in their 401ks is because they just don’t understand them, or they have a huge lack of organized information, so they don’t know where to start.

Even if you don’t have a 401k, I encourage you to read this. Odds are, if you’re a professional, you will have a 401k at some point in your life, or something very similar. These principles can be applied to any type of retirement plan.

Now.. we’re going to work on lack of organized information problem right now.

Your Top 11 401k Questions, Answered

—

1.) What is the difference between a Traditional 401k and Roth 401k?

This is often your very first barrier to enrolling in your 401k. It can be hard to make the decision to save money for the future if you don’t know what you’re investing in.

These designations – Traditional and Roth – mean nothing more than how your money is taxed.

In a Traditional 401k, your money is taxed AFTER you take it out. In the mean time, whatever you put in reduces your tax liability in the year you invest it.

So if you make $50,000 in a given year, and you invest $5,000 in your Traditional 401k, then you will only be taxed at a gross income level of $45,000 for that year.

You’ll pay tax on that $5,000 as you take it out at retirement.

With a Roth 401k, this is exactly the opposite. You pay tax at the time you invest and you owe no taxes on that amount when you decide to take it out. This doesn’t affect your current year tax liability because it has already been taxed when you receive it.

The earnings on both types are not taxed at all, which is why a 401k is so incredibly powerful – because this allows your money to grow tax free.

So, which should you choose?

The answer is – it depends on your tax situation.

You can get more money into a Traditional 401k and often experience higher growth levels because you’re not getting taxed as you deposit it, but it is also taxed when you withdrawal it, so you’ll have to factor that in with your tax planning in retirement.

If you would prefer more predictable taxes, a Roth 401k will allow you to avoid taxes at the time of withdrawal. Basically, you’re betting your tax rates will be higher when you are older.

Two important notes here:

If you get an employer match on your 401k at all, this is taxed like a Traditional 401k deposit, so keep that in mind with what percentage of your 401k balance that is.

It’s also important to remember that this choice isn’t set in stone. You can always swap your choice if your tax situation changes. The money you put in at a certain designation will be taxed the same, but the rest after your switch will be taxed with your new choice.

2.) How much do I need to save?

Since you don’t have a crystal ball (if you do, I would like to borrow it), this is another choice that can really hang you up. How are you supposed to know what the future will bring and how much money you need for it?

It’s a tough question.

The good news is, there is an extremely simple principle-based answer to this situation. This involves initially setting up your 401k for the maximum benefit with the smallest investment on your part.

Some might call this an MED of getting started with your 401k, or minimum effective dose.

Most companies that offer a 401k also offer a 401k match. This is free money that acts as an incentive to participating in the retirement plan. Many companies also use this as a massive benefit to their employees.

Check with your company on what the maximum match is and what you have to deposit to get all of it, and then set your 401k to that percentage (you’ll want to deposit more eventually, but this will help get you started easily and logically).

(Pro Tip: For the next step check out my Kindle Book, Six Figure 401k – Five Steps to Starting Your 401k Off Right, which is free on Amazon from July 1 – July 5, 2015, and less than the price of a nice lunch after that.)

This is usually is something like “we will match 100% of the first 5% you invest” – which basically means if you invest 5% of your gross income, your company will match that for free. They’ll just deposit that exact same amount into your account.

This usually ends up being several thousand dollars per year in most cases and can add up to tens of thousands or hundreds of thousands over time with the compounding effects of money growth over time.

If you don’t deposit up to that level, you are quite literally forfeiting free money.

Again, this isn’t set in stone. You can always adjust this as your financial situation changes, so don’t nitpick over this decision. Just set it up and move on.

If your company does not offer a match, then 5% is a good place to start. If you’re worried about the impact it’ll make on your finances, well, how do you think you’ll feel when you have no money to retire?

I can guarantee you it’ll be a lot worse to have no money when you want to quit working than it will be to have a couple hundred bucks a month less now when you have a steady income.

Trust me here. You’ll adjust. And when your 401k balance and net worth is growing at four to five figures a year, you’ll be glad you did this sooner rather than later.

My 401k makes up a full 1/3 of my current net worth, and that will only grow over time.

3.) What happens to my money when I invest it?

I hear this fear a lot. Many people think that when they invest in a 401k, their money is just gone, and they might not be able to get it back if they choose to switch jobs.

This is completely false.

Any money you invest in your 401k is in a bank account in your name, and your name only. It will not be lumped into a giant government retirement pool, or some union benefit pension fund that you may nor may not see.

The only part you have to wait on is your employer matches. These often have a vesting period of six months to a couple of years, which is completely sane. This is to protect companies from financial losses and help balance their cash flow.

When you first deposit money into your 401k, it’s usually just cash until you set up your investments. Some companies will choose default investments for you, which – unless you work for Google or Apple – you’ll likely want to change because your company has no idea what your unique financial situation is.

After you deposit money into your 401k, you’ll then decide what to invest it in.

4.) What should I invest in?

Each time you get paid, your money is auto-deposited from your paycheck into your 401k. This money is then invested in investments that you choose.

I can’t tell you exactly what to invest in, because I don’t know what your 401k looks like, but I can help to give you some guidelines.

As always, invest at your own risk.

A few simple rules here are:

- If you’re 20-30, you’re probably safe with mostly “growth” type funds. The word “growth” will usually be in the name of the fund. These usually contain shares of many established, yet aggressive companies that have a lot of room to grow. They can be more risky, but they can often pay off big.

- If you’re 30-40, you still want to grow your money quite a bit, but you also want to protect yourself from market selloffs. Take caution against putting everything into growth funds and check out investments that possibly mirror a certain sector, or those that mirror established companies with very large market caps. These would often have “large cap” or “mid cap” in the name.

- If you’re 40-50, you’ll want to start investing a little bit more safely. Check out bond funds to hedge against losses that you may encounter with stock driven funds. You may also want to consider target-date funds at this point, which will help you set up to retire in a certain year, and adjust risk over time for you.

- If you’re 50+, your retirement is hopefully coming soon. You don’t want your money to stop growing, but you don’t want to lose it either. You may want to consider moving a large portion of your assets to investments that are protected against losses, such as bond funds and other types of fixed income funds. This will all depend on how much you have saved, and what your withdrawal rate will be. If you can afford to be 100% safe at this point, then it’s a good idea to do so.

5.) When can I get my money?

At age 59 1/2, you can begin to access the money in your 401k without taking an early-withdrawal penalty. There is also actually a little known exception to this rule that some call the “rule of 55.”

This allows you to access your money at age 55 from your most current employer, on the year you turn 55. You cannot, however, take distributions from a previous employer 401k. It gets complex, so I won’t go too far into this, but feel free to look more into that if you’re thinking about retiring earlier than age 59 1/2.

6.) What are these penalties I keep hearing about?

If you want to access your money before these ages, you can technically access your money from your 401k at any time.

That said, since this is a tax-protected account and you put your money there for a reason (to retire someday) you will have to either pay a small penalty (usually 10%) plus taxes (if it’s not a Roth), or you can take a loan from your 401k balance of up to $50,000, or 50% of the balance of your 401k, whichever is smaller. These loans are usually fairly low interest.

I would highly advise against this however, because once you start viewing your 401k as a bank account that you can access before you retire, the wheels can easily fall off and you’ll have no retirement money left. This is just simple psychology. If you don’t want to spend it, don’t touch it.

I’ve seen this happen to people before and they end up broke when they want to retire. Don’t let this happen to you.

7.) What happens if I change jobs?

This is a great question, because it happens often, especially in today’s world. Those of the Gen Y generation are expected to change jobs every 3-5 years.

The good news is, your 401k money is yours to keep. You can do what is called a “rollover” into an IRA that you manage. In some cases, you can even roll your old 401k into a 401k at your new job. It all depends on the rules of that employer.

There may be some small fees involved in this for the transactions, but they’re usually fairly minimal.

Either way, you keep the vast majority of your money, which would not be the case with a pension fund or some other type of retirement plan that forces you to stay for a certain number of years before being eligible to access it.

Something to take note of is that you might lose a little bit of the money that isn’t vested yet. The employer match dollars we talked about earlier are usually on a delayed vesting schedule. You’ll want to check on this before you make your decision.

8.) How long do I need to save to retire?

The longer you save and invest, the more you can take advantage of compounding interest. The simple answer to this question is “get started as early as possible.”

To be safe, you usually need about 25-30 years to build up enough to retire, depending on your portfolio performance. The longer, the better.

Five years of compounding interest in a 401k can be the difference between a six figure balance and a seven figure balance, quite easily.

If you don’t believe me, play around with this 401k Calculator. You’ll notice by adjusting the “Age of Retirement” cell up and down between 50 and 60, that this makes a massive difference in your ending balance.

This isn’t because of how much you save over time. It’s because of how long your money has had to multiply upon itself.

9.) Should I max out my 401k?

Like I said earlier, the more you can save towards your retirement and still maintain your needs (needs, not wants), the more I believe you should put towards your retirement. We weren’t put on this planet to work our entire lives.

That said, it may not be the best strategy to max out your 401k first.

The reason is because once you deposit money into a 401k, it cannot be accessed without penalty, at least until you’re of age.

However, if you deposit retirement money into a Roth IRA, you can access anything you deposit without a penalty, at any time.

For this reason, a lot of people will first make sure they’re taking maximum advantage of their employer match, then completely max out a Roth IRA ($5,500 at the time of this post), then put the remainder of what they want to save in a 401k.

This allows some flexibility and liquidity with these high dollar accounts if you need it.

Now, should you put the maximum amount in both?

You can currently deposit up to $17,500 in a 401k annually. This is all going to depend on your income and relative spending. If you make $40,000 a year, it’s going to be nearly half of your income to max out your 401k completely.

You may want to think about splitting your investments between your maximum employer match and a Roth IRA. This will allow you some decent flexibility until you’re making more money.

However if you make $80,000 – $100,000+, which a number of Academy Success readers do, you can easily max out a Roth IRA and have plenty leftover to max out a Traditional 401k.

If this sounds nuts, just remember this.

Your retirement savings, or any savings for that matter, shouldn’t be what you have leftover at the end of each month. It should be very intentional. You should be saving first, and spending second.

Otherwise, made money has a nasty way of evaporating, and you’re very likely to have nothing left over at all.

10.) Why shouldn’t I just keep all of my money for now?

Yes, people actually ask this question.

My gut tells me that you probably already don’t like working every single day of your life. If you ever want to escape this life, saving for retirement is a must.

Like I said earlier, no one is going to do this for you.

- Social security will not fund your retirement

- You won’t get an inheritance large enough to retire on

- And you sure as hell aren’t going to win the lottery

- You need a plan

If you don’t want to be a super massive stressed out ball of chaos nearing your death bed when you’re ready to hang up the work clothes, then save now, my friend.

Otherwise you may end up working until the day you die – and that’s an absolute reality for some people.

11.) How much money can I actually save?

Hundreds of thousands, millions, even tens of millions.

The power of compound interest with a balance as large as your 401k is amazing, and this only gets better the earlier you get started.

While you can technically only save $17,500 (+$5,500 with an IRA), that can end up turning into seven, or even eight figures by the time you are ready to hang it up.

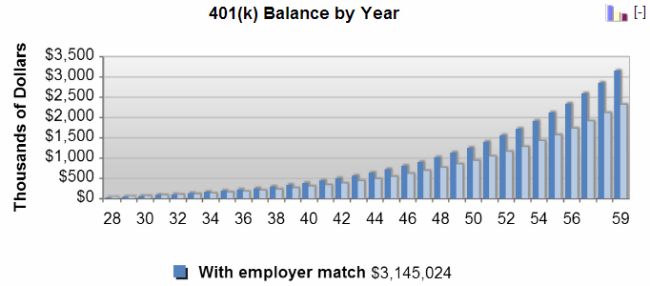

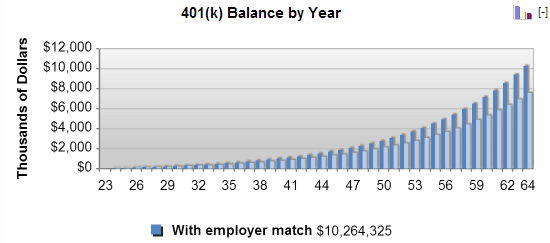

These images represent one person starting at age 28, and investing until age 60, and the next person starting at age 23, and investing until age 65. This is a 10 year difference.

If you’re in your early 20s right now and you’re reading this, first – that’s awesome, and second – I envy you.

This is the power of time and compound interest.

With the same investment amounts, the person who starts in their late 20s and retires at 60 makes $3.1 million, while the person who starts in their early 20s and retires at 65 would make nearly 3x more – over $10 million

This all happens with routine and repeated deposits, and the power of money growth over time.

And the best part is, once you adjust to your 401k investing lifestyle, you won’t even miss that money. It’ll just be a part of life and you’ll be racing towards retirement.

Grab Your Free Upgraded Printable Report

If you’d like a free PDF copy of this blog post, I’ve created an upgraded copy with a nice design that you can download, print out, mark up, and do whatever you would like with.

I’ll also include a copy of my Financial Automation Checklist Collection as a free bonus, which includes two checklists to help you automate your investments, as well as your retirement savings, and a free video showing you how to set up your first automated savings plan!

You can grab that here. Just click below and let me know where to send it!