The Incredible Earning Power of the 401k Quadruple Threat

Today, I want to show you what I call the “quadruple threat” of your 401k, and how these four factors can combine to potentially create millions of dollars of wealth.

Now, I know what you might be thinking right now.

“It can’t be that big of a deal…?”

I thought the same thing when I first got my 401k. My dad always told me that a good retirement plan was one of the biggest differentiators between employers, and to make sure I found a job that had one.

I didn’t think much of it at the time. Retirement just seemed so far off.

But then I started learning how 401k plans work, and the massive advantages to create wealth that would come with them. That’s when I started to understand what he was talking about all of those years. That’s when the 401k quadruple threat was born in my mind.

And like a nerd at a comic book convention, I started getting really excited.

It was at that point when I had this idea. “Wow. I could be a millionaire!”

“Millionaire” …. ? Wait… Wait… Wait a second… Can you really make “millions” with nothing but a 401k?

No way right? That’s what I thought at first too.

But it turns out that the answer is actually a resounding “yes”.

(BTW – Did you know that nearly 50% of people who have a 401k don’t use them? Just makes you wonder… what’s their plan? Don’t let this be you.)

Here we go.

1- Your 401k Is A Certified Tax Bomb Shelter

Both types of 401k plans, Traditional and Roth, have a provision built into them that allows you grow your money tax-free (this is similar to IRAs and Roth IRAs, which you can buy into on your own in addition to your 401k, but that’s for another day).

Where you would normally pay capital gains tax on your money growth (anywhere from 15 – 20% depending on your income, or $200 of every $1000 you gain), you are exempt from this in a 401k plan.

Ok. Big deal… what does that really mean?

Well, this means your money can grow without you having to worry about a ridiculous tax bill when you go to cash it in because you don’t pay tax on it’s earnings.

You can also lower your tax liability now at the same time, saving you money now, and later. This is a beautiful thing.

And even better, if you have access to a Roth 401k, you can deposit after tax dollars, which means you pay absolutely $0 in tax when you withdraw your money. The only thing that is taxed in that situation is contributions from your employer, which we’ll talk about next.

This tax is why there is a maximum limit on what you can contribute. Because otherwise you could just grow all of your money tax-free.

2- Your 401k Gives You 100% Free Money

Some might call this “employer contributions” but I like to call it Free Money, because that’s what it is.

You literally do no extra work for this.

Why would your employer just give you free money? Well… a 401k plan is awesome for employers, because it encourages their employees to save money, and they avoid the need to manage a giant pension fund or some other form of pooled retirement benefit.

Employer contributions are basically their bribe to get you to participate, which works out awesome for you.

For some reason, financial experts like to make this sound really complicated though, using language like “Company XYZ will match 100% of the contributions of the first 5% of the employee salary.”

That’s not exactly easy to understand, and is a big reason why many people don’t take advantage of this HUGE benefit. Complicated language creates a barrier. Don’t let that stop you.

What that basically means is that your employer will match up to 5% of your gross salary, as long as you contribute that much as well.

So let’s say you make $50,000 before taxes. Well if your employer has a 5% match, guess what?

As long as you contribute at least 5% of your gross salary, you get an extra $2,500 from your employer, for no extra work at all – totaling $5,000 a year.

Now that might not sound like a heck of a lot, but consider getting that $2,500 for 30 years.

Over time, that’s an extra $75,000 in your pocket. And that extra $75,000 grows with the rest of your money. Over 30 years, just that tiny little 5% becomes just over $433,000 at a growth rate of 10%.

Not too shabby for something you did absolutely nothing for.

And the crazy part is, all of those people who don’t use their 401ks are completely forfeiting all of that.

Can you see how insane that is!? It blows my freaking mind.

Ok. Now that my rant for that piece of over, let’s talk about how the rest of your money is going to grow.

3- Your 401k Is a Giant Snowball

The base amount of money you save with your 401k isn’t all that much. It’s definitely not enough to retire on. This is where a lot of novice savers go wrong with their thinking.

They think….”Ok, so if I want to be a millionaire, I have to save… $50,000 every year for the next 20 years… ? Wait… there’s no way that’s happening… Why even try…?”

And then they give up before they even get started. This happens SO OFTEN, and I can’t stand it. People give up with investing before even looking into it.

But long-term money growth doesn’t work that way.

A 401k is a long-term investment that builds upon itself over time. It starts small, like a snowball at the top of a huge snowy mountain.

It picks up speed and snow slowly at first as it begins it’s descent down the slope.

Somewhere in the middle, it begins to pick up it’s pace. And as it does, it grabs WAY more snow.

By the time it has passed the middle, the snowball has A TON of momentum, and it barrels it’s way down the mountain, picking up everything it’s path, and growing huge.

Until finally, it reaches the end of the mountain, and what was once a tiny snowball is now a massive boulder of cash, and enough to live on for the rest of your life.

Using our example from above, that snowball could be yours.

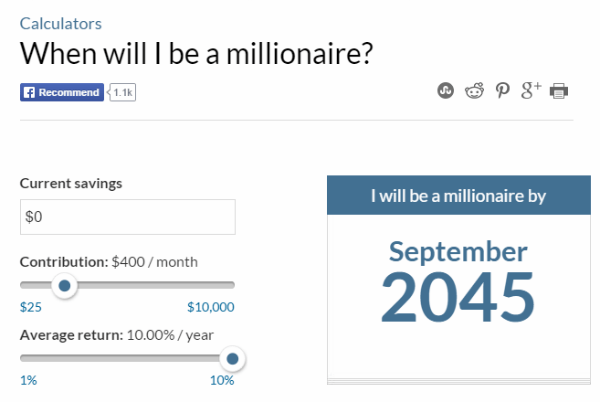

Let’s say you’re 35, and you’re saving that 5% and getting that 5% match. That’s $5 G’s a year, or about $415 a month that you’re saving.

According to CNN’s Millionaire Calculator, even if you have $0 right now, you can still be a millionaire by the time you’re 65.

Why anyone in their right mind would pass that up, I have no idea.

I’m not trying to be mean here. I’m just trying to open up your eyes to the possibility of what is right in front of you.

Even a small amount of money, which will be barely noticeable to you after 56 days of fully adjusting your habits, (yes that number is real) that is consistently invested over the course of your life, can add up a HUGE amount of wealth.

You can argue with me, but you can’t argue with math 🙂

The first three of these you can find anywhere, but this next area of 401k’s is something that is rarely written about.

So let’s check out the last piece of the 401k quadruple threat, which I think is the most awesome of all, because it has to do with the area that so many people struggle with when it comes to money… human behavior.

4 – Your 401k Can Run on Autopilot

As humans, we only have a certain amount of discipline available to us at any given time. Our habits, routines, and ingrained behaviors allow us to operate without having to blow through our discipline and decision-making reserves in the first 30 minutes of the day.

As an example of this, just think of the last time you did something like skip a workout after you had a stressful day. Your discipline for that day was exhausted and you skipped an area of you personal development because of it.

The problem with this is, when attempting to change a behavior such as spending, it’s very difficult to do because we are faced with the discipline of spending choices dozens of times per day.

What’s the answer to that challenge?

AUTOMATION

Automation allows you to save without having to think about it, and the rest is left over for you to do with as you please (spend responsibly, my friend).

Pay yourself first, as they say.

Your 401k has automation built in.

It started with just automated contributions from your paycheck, which was awesome enough in itself.

Then things like target-date funds, and automated rebalancing (you’ll learn about those in the course) were introduced, and it basically made it so the entire wealth creation process can happen 99% on autopilot.

This is a HUGE DEAL, because it means you can literally set up your 401k one time, check in on it once or twice a year, and create the wealth you want to do everything you desire when you retire (I honestly didn’t mean to rhyme that :)).

These four factors together combine to provide you the ability to create an incredible amount of wealth, essentially on autopilot.

There are few other financial vehicles or systems that allow you to do this.

But you have to take the action to do it first, and that does take a little bit of work on your part, which will be handsomely rewarded when executed correctly.

And that’s exactly why I created this training material

Because there are so many people out there such as yourself, that have access to a 401k, but have just gotten it dumped on them and don’t know what to do in order to maximize it’s value.

When I started with mine, I was in the same frustrating situation, and I don’t want you to go through the same hundreds of hours of research and labor that I did to learn what I know now.

I want to make it easy on you, and the training you’re getting right is one of the first steps you’re taking in that direction.

I am the author of this art piece. This photography was posted on my website under the creative commons license. You have used my image without any permission, and without attribution. It is like stealing. Remove this image immediately from this webpage, or be cursed